Business Law Specialists

Debt Collection.

Debt collection can cover a wide range of work and potential costs depending mainly on:

- the volume of paperwork that we need to review to establish if you have a claim and prove that claim;

- the volume of paperwork that the other party provides to dispute your claim;

- the technical complexity of the legal issues involved in your claim;

- the volume of correspondence generated by the other side in discussions/ negotiations in relation to the claim; and

- the extent to which proceedings in relation to the claim is defended by the other party.

It is a common misunderstanding that if you obtain a Court Judgment then you will be paid. THIS IS NOT THE CASE. A Court Judgment merely means that the Court has adjudicated that you are owed money by the debtor. You still need to “enforce” that judgment (obtain money from the debtor). For this reason, we like to establish from the start of our working relationship whether or not the debtor will ever have the funds to pay you regardless of the merits of your claim against the debtor.

Debt collection against an individual is more costly and complex and time consuming than against a limited company as extra “pre-action protocols” need to be followed.

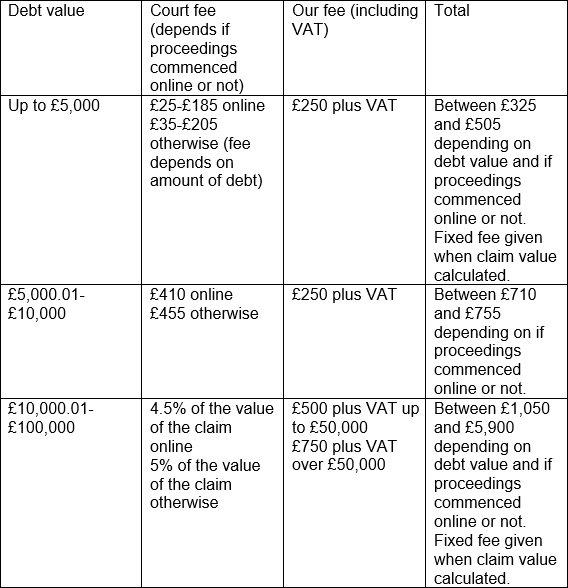

Range of fixed fees for a business to business (limited company) debt that is undisputed:

Court Claims

These costs apply where your claim is in relation to an unpaid invoice which is not disputed and enforcement action is not needed.

If the other party disputes your claim at any point, we will discuss any further work required and provide you with revised advice about costs if necessary, which could be on a fixed fee (eg if a one off letter is required), or an hourly rate if more extensive work is needed.

Anyone wishing to proceed with a claim should note that:

- the VAT element of our fee cannot be reclaimed from your debtor;

- the majority of our costs cannot be reclaimed from your debtor if your claim is for under £10,000 (the “Small Claims” limit);

- for successful claims over £10,000 a significant amount of our costs (usually c. 75% to 100%) can be recovered;

- interest and compensation may take the debt into a higher banding, with a higher cost; and

- if you lose a Court claim, you are likely to face liability to pay the costs of the other side, which could be significant if the claim is for over £10,000.

The costs quoted above are not for matters where enforcement action, such as the bailiff, is needed to collect your debt.

Our fee includes:

Taking your instructions and reviewing up to 5 A4 pages of documentation (if there is further documentation that needs to be reviewed then we will give a fixed price for this review when the documents are supplied so we know the volume of paperwork)

Undertaking appropriate searches (if any) on the debtor

Sending a Letter Before Action

Co-ordinating payment and sending any cheque from the debtor on to you or if the debt of not paid drafting and issuing a claim (note we do not hold client funds so debtor payments need to be made directly to you and not this firm)

Where no Acknowledgement of Service or Defence is received, applying to the Court to enter Judgment in Default

When Judgment in default is received, write to the other side to request payment (additional Court cost ranging from £22 to £35 depending on the debt value)

If payment is not received within 28 days of judgment, providing you with advice on next steps and likely costs

Matters usually take from 1 week to 12 weeks from receipt of instructions from you to receipt of payment from the other side, depending on whether or not it is necessary to issue a claim

This is on the basis that the other side pays promptly on receipt of Judgment in Default

If enforcement action is needed the matter will take longer to resolve

Please remember that if the debtor is unable to pay you will receive no payment and will still have to pay our costs and the Court fees

Experience

Your debt collection work will be done by or under the direct supervision of Andrea Knox or Philip Roberts

Andrea Knox is a dual qualified Solicitor and Licensed Insolvency Practitioner with over 20 years of debt collection experience. Andrea qualified as a Solicitor in 1998.

Philip Roberts is a specialist qualified Commercial Solicitor with over 4 years of debt collection experience. Philip qualified as a Solicitor in 2016.

Talk To Us Today

Knox Commercial & Insolvency Solicitors, 20 Wynnstay Road, Colwyn Bay, LL29 8NF![]()

Knox Insolvency, Knox Commercial and D£BTFAIR are trading names of Knox Insolvency Limited

which is authorised and regulated by the Solicitors RegulationAuthority.

Solicitors Regulation Authority Firm No: 592107

- VAT No: 974 0099 04

- Knox Insolvency Ltd, Company Registration No: 07413459

Privacy Policy | Site managed by Jenlu Limited